Related Articles

“`html

Analysis: Pakistan’s Agriculture Tax Reform Stalls at the Farm Gate

The quest for fiscal sustainability in Pakistan continues to face formidable challenges, particularly in the critical area of agricultural income taxation. Despite a concerted effort to introduce a unified agriculture income tax (AIT) regime, the initial year of implementation (FY2025-26) has revealed a stark and disappointing reality: provincial tax authorities collected a mere 2 percent of the agricultural income declared by taxpayers. This significant shortfall not only undermines the reform’s ambition but also exposes deep-seated structural issues and political impediments within Pakistan’s economic framework.

The News: A Disappointing Debut for Unified AIT

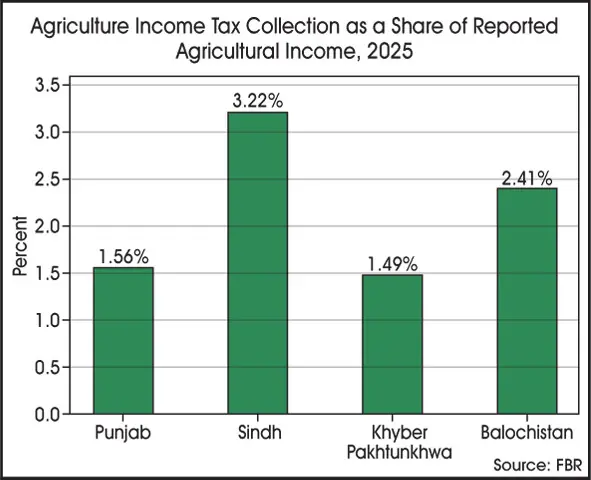

Provisional data for fiscal year 2025-26 paints a grim picture for Pakistan’s landmark agriculture income tax reform. While taxpayers across the four provinces declared a substantial Rs306 billion in agricultural income, provincial governments collectively managed to collect only Rs5.62 billion in AIT. This translates to an abysmal collection ratio of just 1.8%, falling far short of expectations and highlighting a significant gap between policy design and practical enforcement.

Introduced last year as a key component of a fiscal restructuring program, partially backed by the International Monetary Fund (IMF), the unified AIT framework aimed to harmonize tax rates and legal structures across provinces. However, divergent implementation strategies have emerged: Sindh aligned its super tax with federal rates while abolishing advance tax; Punjab increased advance tax rates; and Khyber Pakhtunkhwa (KP) abolished super tax altogether, retaining a zone-based fixed tax per acre. Balochistan’s policy details remain opaque, shrouded in a lack of public fiscal reporting.

Experts attribute this failure to deeply entrenched issues, including the overwhelming political influence of large landowners, weak administrative capacity, and a pervasive lack of political will at the provincial level. As former chief economist Dr. Mohammad Ahmed Zubair notes, “Provincial governments are effectively captured by the landed class, so any attempt to tax agricultural income becomes a tax on the governing coalition itself.”

Background: The Enduring Challenge of Agricultural Taxation in Pakistan

Agriculture is the backbone of Pakistan’s economy, contributing a significant portion to its Gross Domestic Product (GDP) and employing a substantial segment of its workforce. Despite its economic weight, the sector has historically remained undertaxed, creating a glaring inequity within the national tax system. This historical context is crucial for understanding the current challenges.

Constitutional Framework and Fiscal Federalism: Under Pakistan’s constitution, agriculture income tax falls under provincial jurisdiction. While seemingly straightforward, this division of power has historically been a source of contention and inefficiency. Each province has the autonomy to design and implement its AIT laws, often leading to inconsistencies, loopholes, and an inability to create a cohesive national tax strategy for the sector.

The Landed Elite’s Influence: Pakistan’s political landscape has long been dominated by powerful feudal landlords and large commercial farmers. This influential class often forms the core of provincial political power structures, making any substantial attempt to tax agricultural income a direct challenge to their vested interests. Reforms are frequently diluted or rendered ineffective due to strong lobbying and political resistance, turning agricultural land into a de facto tax shelter for the wealthy.

Pressure for Fiscal Reform: In recent years, successive governments have faced immense pressure from international lenders, particularly the IMF, to broaden the tax base and mobilize domestic resources. Addressing the undertaxed agricultural sector is consistently highlighted as a critical area for reform to alleviate Pakistan’s chronic fiscal deficits and reduce reliance on borrowing. The “unified” AIT regime was a direct response to these demands, aimed at finally bringing equity and revenue to this crucial sector.

Economic Disparities and Revenue Shortfalls: The continuous failure to effectively tax agricultural income places an undue burden on other sectors, such as industry, services, and salaried individuals, who bear a disproportionately higher tax load. This not only exacerbates income inequality but also limits the fiscal space available to provincial governments for crucial development projects, public services, and infrastructure investment, particularly in rural areas.

Impact on Pakistan: Deeper Crises and Eroding Trust

The stalled progress on agriculture income tax reform carries significant repercussions across multiple facets of Pakistan’s socio-economic and political landscape:

- Exacerbated Fiscal Crisis: Provinces are struggling to meet their own revenue targets, making them increasingly reliant on federal transfers. This perpetuates the national fiscal crisis, as the federal government itself grapples with budget deficits and a massive debt burden. The inability to tap into a major revenue source leaves provinces with insufficient funds for development and public services, hindering progress.

- Jeopardized IMF Programs: The IMF and other international financial institutions consistently advocate for broadening Pakistan’s tax base. The failure to significantly improve AIT collection could be perceived as a lack of commitment to fiscal reforms, potentially jeopardizing ongoing or future IMF bailout packages. This could lead to stricter conditionalities, further austerity measures, or even a breakdown in financial support, pushing Pakistan deeper into economic instability.

- Widening Socio-Economic Inequality: When the affluent landed elite effectively evades its fair share of taxes, the burden invariably falls on the common citizen through indirect taxes, inflation, and a lack of public services. This fuels social discontent, deepens income inequality, and undermines public confidence in the fairness and effectiveness of the state’s institutions.

- Weakened Governance and State Capacity: The persistent failure to implement AIT effectively highlights a critical deficit in state capacity and governance. It demonstrates the inability of the state apparatus to enforce its own laws against powerful vested interests, eroding public trust and the rule of law. The “patwari culture” and weak land records further underscore the systemic administrative challenges.

- Distorted Economic Incentives: An undertaxed agricultural sector can inadvertently create distorted economic incentives. It may encourage capital to flow into agriculture as a tax shelter rather than into other, more heavily taxed sectors that might offer higher productivity or employment potential.

Analysis: The Anatomy of a Stalled Reform

The gap between declared agricultural income and actual tax collection is not merely an administrative oversight; it is a complex issue rooted in political economy, administrative deficiencies, and a lack of coherent policy implementation.

Root Causes of Failure:

- Political Entrenchment of Landowners: This is arguably the most significant hurdle. Provincial legislatures are often dominated by individuals from land-owning families. Asking them to enforce a stringent AIT is akin to asking them to tax themselves, which naturally faces strong resistance. The “IMF pressure exposes the contradiction but cannot resolve it,” as highlighted by Dr. Zubair.

- Administrative Weaknesses:

- Outdated Land Records: Many provinces still rely on archaic land registration systems, making it difficult to accurately identify land ownership, assess farm size, and verify income. While digitisation initiatives are underway, their impact is yet to be fully realized.

- Lack of Modern Assessment Tools: Assessing fluctuating farm incomes, accounting for input costs, and verifying losses require sophisticated administrative machinery that many provincial revenue departments lack.

- “Patwari Culture” and Corruption: The traditional land revenue system, often associated with corruption and patronage, hinders transparent and fair tax collection.

- Divergent Provincial Implementation: Despite a “harmonised legal framework,” provinces have adopted vastly different approaches. Sindh abolished advance tax, while Punjab increased it. KP eliminated super tax for high earners, a move counter to the spirit of progressive taxation. This lack of uniformity creates loopholes and makes holistic enforcement challenging, eroding the “unified” aspect of the reform.

- Data Gaps and Lack of Integration: Incomplete crop records, inconsistent land data, and a lack of integration with other databases (like bank transactions, mill records for growers) make it difficult to ascertain actual agricultural income accurately.

- Focus on Small Farmers vs. Large Landowners: While it is crucial to protect small farmers, the current system often fails to effectively tax large commercial farms and absentee landlords who derive substantial incomes. The exemptions and thresholds, if not carefully designed and enforced, can disproportionately benefit the wealthy.

Path Forward: Towards Effective AIT

To move beyond the current deadlock, a multi-pronged strategy is essential:

- Sustained Political Will: True reform requires a genuine political commitment from provincial leaderships to confront vested interests. This may necessitate a broader national consensus on the importance of equitable taxation.

- Comprehensive Digitisation and Data Integration: Investing heavily in modernizing land records, using technologies like satellite imagery and drone surveys (as Sindh is attempting) to verify cultivated land, and integrating data from various sources (banks, commodity markets, agricultural mills) can significantly improve assessment accuracy and reduce evasion.

- Strengthening Provincial Tax Authorities: Professionalizing revenue boards, enhancing their administrative capacity, providing adequate resources, and ensuring their autonomy from political interference are crucial. Training tax officials in modern assessment techniques is also vital.

- Progressive and Fair Taxation: The AIT system must be designed to effectively tax large commercial farmers and absentee landlords while safeguarding genuine small landholders. This means revisiting exemption thresholds, slab rates, and super tax provisions to ensure they target the wealthy.

- Transparency and Accountability: Publicly accessible data on declared income, collected tax, and enforcement actions can foster accountability and build public trust. Regular audits and robust penalty mechanisms are also necessary.

- Harmonized Implementation, Not Just Legislation: Provinces must work towards not just a common legal framework, but also a common strategy for implementation, minimizing loopholes that arise from divergent policies.

The current struggle with agriculture income tax is more than just a fiscal challenge; it is a test of Pakistan’s resolve to address deep-seated inequalities, strengthen its institutions, and build a truly equitable and sustainable economy. Without fundamental changes in political will and administrative capacity, the vision of a broad-based, fair tax system will continue to remain stalled at the farm gate, perpetuating the nation’s fiscal vulnerabilities.

“`